While a trade surplus is usually seen as a positive sign of economic health because it indicates a country is exporting more than it imports, a persistent and large trade surplus, especially by major global players like China, has also generated geopolitical and economic tensions worldwide.

Interestingly, in the decades preceding China’s emergence as a major exporter, from the end of World War II to the early 1970s, the United States ran trade surpluses, primarily due to its industrial strength and its role as a key exporter in the global market —a position China has only recently assumed.

The issue of trade surplus is now becoming the new nuisance in global affairs. Those who benefit from it support it; others protest. However, the discussion of this topic arises from actions by US President Trump, who is attempting to manipulate trade tariffs to influence global trade in favour of the American economy. While a trade surplus is usually seen as a positive sign of economic health because it indicates a country is exporting more than it imports, a persistent and large trade surplus, especially by major global players like China, has also generated geopolitical and economic tensions worldwide. A recent US Treasury report accused China of disrupting the global economic balance through its substantial trade surplus. This article critically examines the financial mechanisms behind trade surpluses, the strategic narratives of developed nations, and the counter-narratives of developing economies, with a particular focus on China.

The latest semi-annual US Treasury report (June 2025) did not label China as a currency manipulator but criticised its lack of transparency in managing the renminbi. Instead, it added countries such as Ireland and Switzerland to its “monitoring list” based on trade surplus and intervention metrics. The report highlights China’s opaque exchange rate practices and suggests that intervention through state tools (e.g., sovereign wealth funds) should be more closely monitored.

Western media and think tanks argue that China’s surplus fuels its industrial oversupply, causing global spillovers and structural trade imbalances. This has harmed local industries in emerging economies by flooding markets with cheap Chinese goods made in factories connected to the Belt and Road Initiative. As a result, many of these countries are now imposing anti-dumping duties to safeguard their domestic industries.

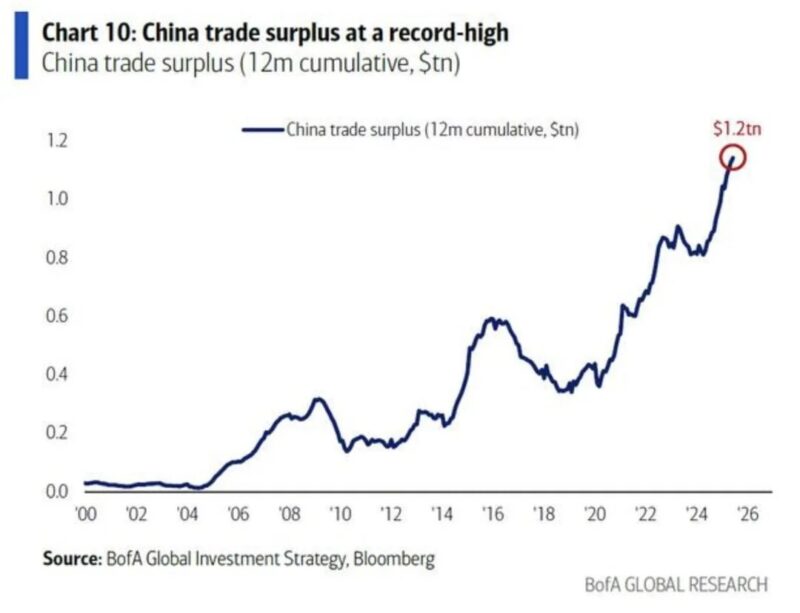

China’s larger economic footprint means its external balance continues to significantly influence trading partners.

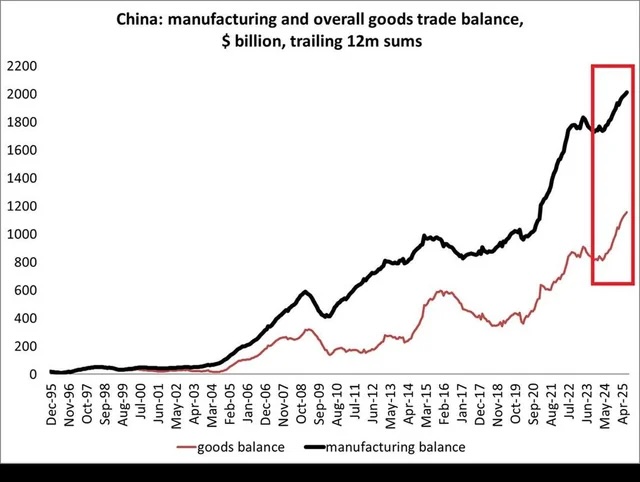

For China, a trade surplus serves both as a consequence and a policy. The IMF contends that China’s surplus mainly stems from internal macroeconomic factors — such as weak household consumption and excess industrial capacity — rather than intentional export strategies or outright manipulation. Although this surplus rate is lower than at the peak of the “China shock” in the 2000s, China’s larger economic footprint means its external balance continues to significantly influence trading partners. IMF models suggest that weak domestic demand — driven by property downturns and low consumer confidence — has caused a decline in consumption in China and has pushed the real renminbi lower, which in turn enhances exports. This has further amplified the trade surplus.

However, Western policymakers and scholars argue that Beijing’s industrial model, underpinned by subsidies and exchange rate policies, amplifies this surplus into a global oversupply and trade friction. Brookings researchers describe this as a “mercantilist trade policy,” characterised by low domestic consumption, state-driven subsidies, and a focus on exports. The resulting surplus—now larger relative to global GDP than during the 2008 peak—puts pressure on trading partners despite US tariffs that have failed to reduce the bilateral trade deficit.

Statistical Distortions: “Missing Imports”

The most revealing statistic is that from 2018 to 2024, official US data revealed a $66 billion reduction in imports from China, while Chinese records indicated a $91 billion increase in exports to the US, a discrepancy of $157 billion. Much of this is due to the US de minimis rule, which permits parcels valued at under USD 800 to enter the country duty-free and bypass detailed customs reporting. E-commerce giants like Temu and Shein exploit this loophole, and 1.36 billion de minimis parcels entered the US market in 2024 alone, most of which originated from China. This underreporting skews trade data, underestimating China’s market reach and downplaying the structural impact of the surplus.

Global Spillovers and E-commerce Consequences

These surplus-driven shipments have severely impacted U.S. domestic retailers. However, bricks-and-mortar firms face import duties, labour regulations, intellectual property standards, and environmental rules. They cannot compete with low-value imports, which are not subject to duties or other regulations. Recent changes in U.S. policy have directly addressed the de minimis loophole, and an exemption for low-value Chinese imports was removed as of 2 May 2025, causing parcel duties to rise to 145%. This has caused small U.S. retailers to halt shipments, and platforms like Temu have been using local warehouses to circumvent fees, only to have the policy to be temporarily rolled back on May 14, highlighting the unstable political climate surrounding e-commerce regulation.

Impact on Emerging Economies

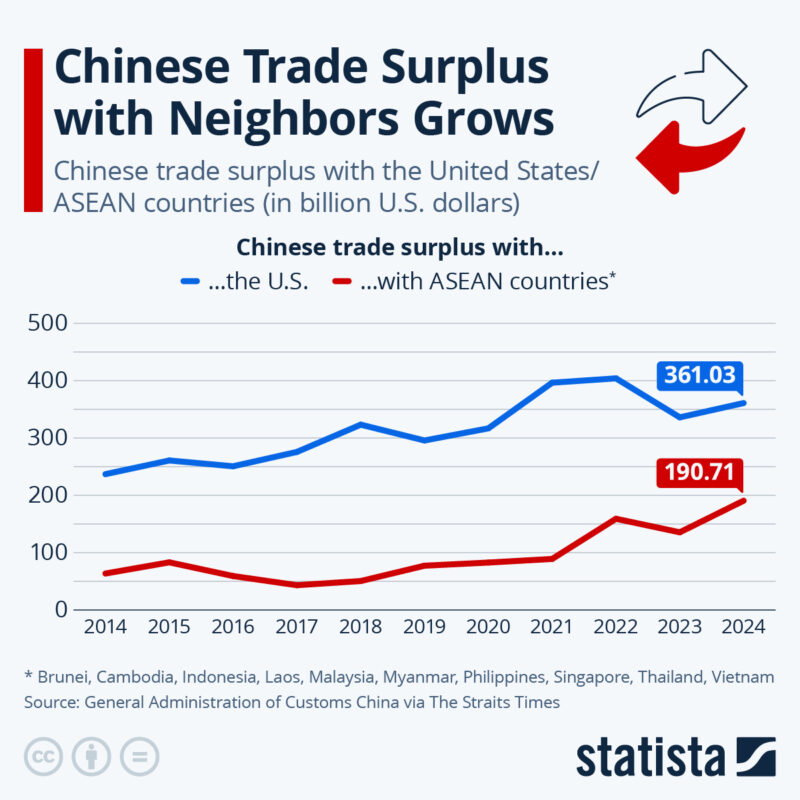

Developing countries are increasingly feeling the impact of China’s surplus-led export model. According to the World Bank, two-thirds of developing economies are expected to see their GDP growth slow from 4.2 per cent to 3.8 per cent by 2025, due to ongoing trade frictions, particularly between the US and China. Inexpensive Chinese goods, whether cheaper solar panels, electronics, or textiles, also pose a threat to emerging markets, and many are fighting back with anti-dumping duties and trade defence measures. At the same time, countries like Brazil, Indonesia, South Africa, and India have imposed tariffs, launched dumping investigations, and reconsidered their trade dependencies. Even countries that are traditionally aligned with China are concerned about the surging Chinese exports. An additional concern is that FDI in developing countries has declined to its lowest level since 2005, reaching just $435 billion in 2023. There is a risk that investment will fall further, raising concerns about investment, infrastructure, and poverty reduction.

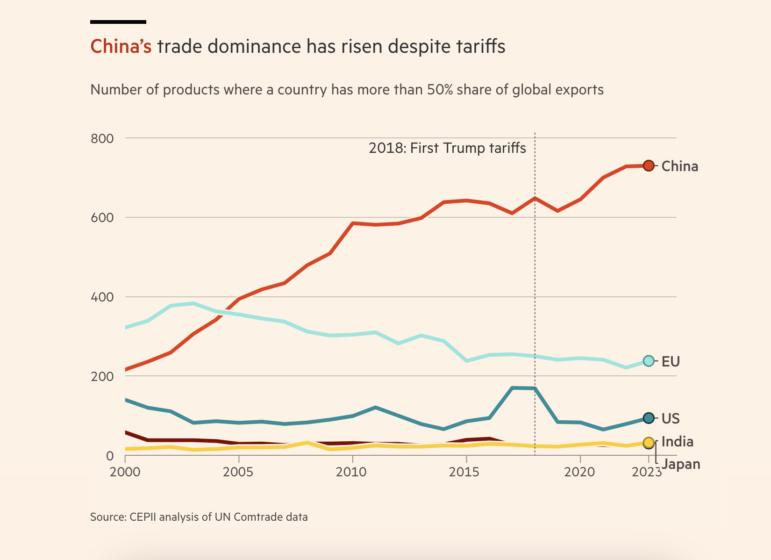

The Times article explains that Donald Trump’s tariffs did not reduce Chinese imports. Even with highly aggressive tariffs, the share of U.S. imports from China decreased by only 7 to 8 percentage points from 2018 to 2024, although industry estimates suggest that the actual fall in Chinese-origin goods entering U.S. supply chains is smaller (perhaps around 3 to 4 percentage points), due to relabelling and third-party routing.

This raises stark questions about the effectiveness of the counter-tariff cycle. The overall outcome of this tariff war is simply a confusing and panicked state of affairs. The Times article explains that Donald Trump’s tariffs did not reduce Chinese imports. Even with highly aggressive tariffs, the share of U.S. imports from China decreased by only 7 to 8 percentage points from 2018 to 2024, although industry estimates suggest that the actual fall in Chinese-origin goods entering U.S. supply chains is smaller (perhaps around 3 to 4 percentage points), due to relabelling and third-party routing.

Theoretical perspectives

Dependency Theory and the Prebisch–Singer Hypothesis argue that developing countries experience declining terms of trade because they focus on primary goods, whereas industrialised nations retain advantages in high-value manufacturing. However, China has challenged this idea by dominating global markets in both primary and advanced products. As a result, we might reasonably conclude that even rising industrial powers, when driven by surplus, tend to uphold the global structures of dependency. Models like Unequal and Ecologically Unequal Exchange demonstrate how trade surpluses frequently involve a systematic undervaluation of labour and environmental costs in poorer countries, redirecting wealth to the Global North.

These theories emphasise how global trade undervalues labour, worsens resource extraction, and causes environmental degradation, thereby transferring wealth from peripheral to core countries. Research suggests that Chinese-led global supply chains contribute to environmental damage and resource depletion in exporting countries, externalising ecological costs, which worsens the structural disadvantages for those nations. China’s GVC-enabled export surge often externalises ecological costs to commodity-exporting nations.

Macroeconomic accounting theory states that a capital account deficit indicates a trade surplus, which means that for China, this results in capital inflows. Consequently, China needs to impose tight controls on its currency to maintain financial stability. With a current account surplus of approximately 3% of GDP, global capital flows, combined with managed exchange rates and the accumulation of foreign reserves—mainly US Treasuries—demonstrate structural policies designed to keep the renminbi weak and direct money into Western securities.

The current trade environment is shaped by negotiation frameworks, such as the US–China truce, and tools, such as WTO rules and anti-dumping procedures. However, the US is now expanding its pressure on Europe, targeting its large goods surplus and digital tax regimes in an effort to rebalance trade.

Global Debate

IMF chief economist Pierre Olivier Gourinchas emphasised that “external balances are determined by macroeconomic fundamentals, not the link to trade and industrial policy, which is more tenuous”. The IMF analysis from the spring meetings similarly implies that internal imbalances (such as differences in savings and investment) influence external current account outcomes, and that China’s surplus reflects its high savings rate, low consumption, and industrial overcapacity. Therefore, while US officials describe China’s trade surplus as a sign of mercantilist excess, IMF analysis reminds us that external imbalances are a reflection of underlying macroeconomic divisions: in China’s case, a high savings rate, low consumption, and industrial overcapacity.

Inderjit Gill, Chief Economist and Senior Vice President for Development Economics at the World Bank, said: “In the rest of the world, the developing world is now a development-free zone.”

Surplus narratives are tools of structural power: while developed nations try to portray surplus as distortion, dumping, and manipulation to justify tariffs, subsidies, and monitoring, developing countries aim to reframe them as ecological exchange and dependency to highlight systemic inequalities

Growth in developing economies, which has ratcheted down from 6 per cent in the 2000s to 5 per cent in the 2010s, and then to less than 4 per cent in the 2020s, mirrors the decline in global trade growth, from 5 per cent in the 2000s to around 4.5 per cent in the 2010s, and below 3 per cent in the 2020s. This illustrates the bilateral nature of the trade surplus. First, fundamentally, surplus narratives are tools of structural power: while developed nations try to portray surplus as distortion, dumping, and manipulation to justify tariffs, subsidies, and monitoring, developing countries aim to reframe them as ecological exchange and dependency to highlight systemic inequalities.

China promotes an alternative narrative about its surplus, arguing that it stems from genuine investment, state-led development, and economies of scale, rather than protectionism or currency manipulation. Belt and Road infrastructure is presented as development, not geopolitical trap – although critics raise concerns of “debt-trap diplomacy”.

Interestingly, in the decades preceding China’s emergence as a major exporter, from the end of World War II to the early 1970s, the United States ran trade surpluses, primarily due to its industrial strength and its role as a key exporter in the global market —a position China has only recently assumed.

A paper by Robert Stehrer titled “What Is behind the US Trade Deficit?” published in ‘The Vienna Institute for International Economic Studies’ (WIW), traces the historical US trade deficit back to the 19th century and places it in a global context. A reading of it would show a broader narrative at play.

Policy Roadmap

Stricter transparency rules are essential to close statistical loopholes and create a level playing field by mandating the disclosure of foreign exchange interventions and de minimis trade flows (such as e-commerce transactions below US$800). These flows can artificially keep a country’s exports cheap and imports expensive, thereby inflating its trade surplus. Countries with persistent surpluses (exceeding 3% of GDP) should participate in a dialogue-based “Global Adjustment Protocol” that includes concessional finance for structural reforms, aiming to strike a balance between conditionality and developmental needs.

One crucial step in this direction would be to include a green surplus index as part of a Green Current Account Score, which measures environmental degradation and natural resource depletion, thereby aligning surplus behaviour with sustainability goals.

The urgent need is for reform of international organisations, liberating the IMF and WTO from Western dominance, transforming them into genuinely global entities or replacing them with organisations like the BRICS bank (NDB) and AIIB. Additionally, they should be empowered with greater authority to monitor global imbalances and suggest corrective measures, such as managing capital flows instead of imposing unilateral tariffs. This would help streamline WTO procedures, reducing delays, and defend policy space—such as supporting trade defence measures (anti-dumping duties, safeguards) by emerging economies.

Conclusion:

This article argues, through an economic analysis of current trade affairs, how hegemonic powers manipulate the political landscape. Trade surpluses are not merely economic aggregates—they are narrative tools in international power politics, with developed countries portraying surpluses as dumping or currency manipulation to justify tariffs and regulatory barriers. Conversely, surplus nations (both developed and emerging) describe their surpluses as the result of sound investments, economies of scale, and effective state guidance.

From the macroeconomic surplus in the economy to the underreported e-commerce inflows, the reality of modern trade imbalances is far more complex than what mercantilist rhetoric suggests. An analysis of China’s experience demonstrates this point. The next phase of global trade reforms should emphasise transparency, robust multilateral regulations, and ecological responsibility. Beyond mercantilist rhetoric, there is a need for systemic frameworks that accurately reflect economic realities and sustainable goals—only then can tensions caused by surpluses be managed in a balanced and lasting manner.

References:

- Financial Times. “The US and IMF Disagree About China. That’s a Problem.” Financial Times, accessed June 23, 2025. https://www.ft.com/content/ff1f35b9-2ccf-4247-9bcd-a9c931b63c5b.

- International Monetary Fund. “Press Briefing Transcript: World Economic Outlook, Spring Meetings 2025.” IMF, April 22, 2025. https://www.imf.org/en/News/Articles/2025/04/22/tr-04222025-weo-press-briefing.

- Meltzer, Joshua P., and Margaret M. Pearson. “How the US Should Address Chinese Overcapacity and Its Impact on International Trade.” Brookings, December 19, 2024. https://www.brookings.edu/articles/how-the-us-should-address-chinese-overcapacity-and-its-impact-on-international-trade.

- Reuters. “US Finds No Currency Manipulators, Adds Ireland, Switzerland to Monitoring.” Reuters, June 5, 2025. https://www.reuters.com/world/china/us-finds-no-currency-manipulators-adds-ireland-switzerland-monitoring-2025-06-05.

- The Wall Street Journal. “The US and IMF Disagree About China. That’s a Problem.” Wall Street Journal. Accessed June 23, 2025. https://www.wsj.com/economy/global/the-u-s-and-imf-disagree-about-china-thats-a-problem-7ab5fca8.

- US Department of the Treasury. Report to Congress: Macroeconomic and Foreign Exchange Policies of Major Trading Partners of the United States. June 2024. https://home.treasury.gov/system/files/136/June-2024-FX-Report.pdf.

Feature Image Credit: Aljazeera.com

Graphs Credits: Reddit; Financial Times; Statista